With a market cap of $119 billion, California-based Prologis, Inc. (PLD) is the world’s largest industrial real estate investment trust (REIT), specializing in logistics facilities, including warehouses, fulfillment centers, and distribution hubs. Headquartered in San Francisco, the company owns and manages a global portfolio spanning nearly 1.3 billion square feet across about 20 countries, serving over 6,500 customers, including major retailers, e-commerce players, and logistics providers.

Companies worth $10 billion or more are generally described as "large-cap stocks." Prologis fits right into that category, with its market cap exceeding this threshold, reflecting its substantial size, influence, and dominance in the industrial REIT industry. Positioned in high-growth, high-barrier markets and benefiting from structural trends like e-commerce expansion and supply-chain modernization, Prologis is widely recognized as the global leader in logistics real estate.

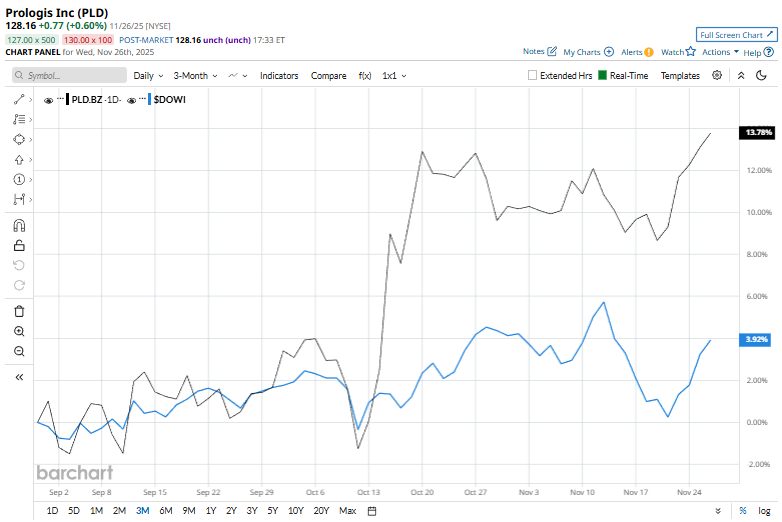

PLD stock touched its 52-week high of $129.28 in the last trading session and has gained 15.1% over the past three months, notably outperforming the Dow Jones Industrial Average’s ($DOWI) 4.4% rise over the same time frame.

Prologis has outperformed the Dow Jones over the longer term as well. PLD stock prices have gained 21.3% on a YTD basis and 10.3% over the past 52 weeks, compared to $DOWI’s 11.5% gains in 2025 and 5.7% surge over the past year.

To confirm the uptrend, PLD has climbed above its 50-day and 200-day moving averages since early August.

On Oct. 15, Prologis reported its third-quarter earnings, and its shares popped 7.3%. The company delivered EPS of $0.82 and core FFO of $1.49, marking a 4.2% increase year over year, while total revenue climbed 8.7% to $2.2 billion. Strong demand for industrial real estate and solid leasing activity pushed occupancy to 95.3%, and same-store net operating income rose 3.9% on a net-effective basis and 5.2% on a cash basis. Leasing momentum remained exceptional, with a record 62 million square feet signed, while rental growth continued to accelerate, posting nearly 49% net-effective rent change and about 29% on a cash basis.

Meanwhile, PLD has outperformed its peer, EastGroup Properties, Inc.’s (EGP) 12.9% uptick in 2025 and 5.3% return over the past year.

Among the 24 analysts covering the PLD stock, the overall consensus rating is a “Moderate Buy.” Its mean price target of $130.65 suggests a 1.9% upside potential from current price levels.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- This AI Dividend Stock Is a Buy Even as the S&P 500’s Yield Falls to Dot-Com Lows

- Have You Heard of the ‘Wheel’ Strategy? These 3 Unusually Active Stocks to Buy Can Get You Started

- 3 Buy-Rated Dividend Aristocrats Easily Beating Inflation

- ‘Insatiable’ Demand Is Powering This ‘Picks and Shovels’ AI Stock up 245%. Should You Buy It Here?